Boston Metal’s strongest near-term case is no longer green steel

Boston Metal has spent years being associated with one of heavy industry’s most ambitious climate goals: making iron and steel without coal. Its core technology, molten oxide electrolysis, was framed as a way to use electricity to reduce metal oxides directly, producing oxygen instead of carbon dioxide. That remains the company’s defining concept, and it is still one of the more technically intriguing routes in industrial decarbonization.

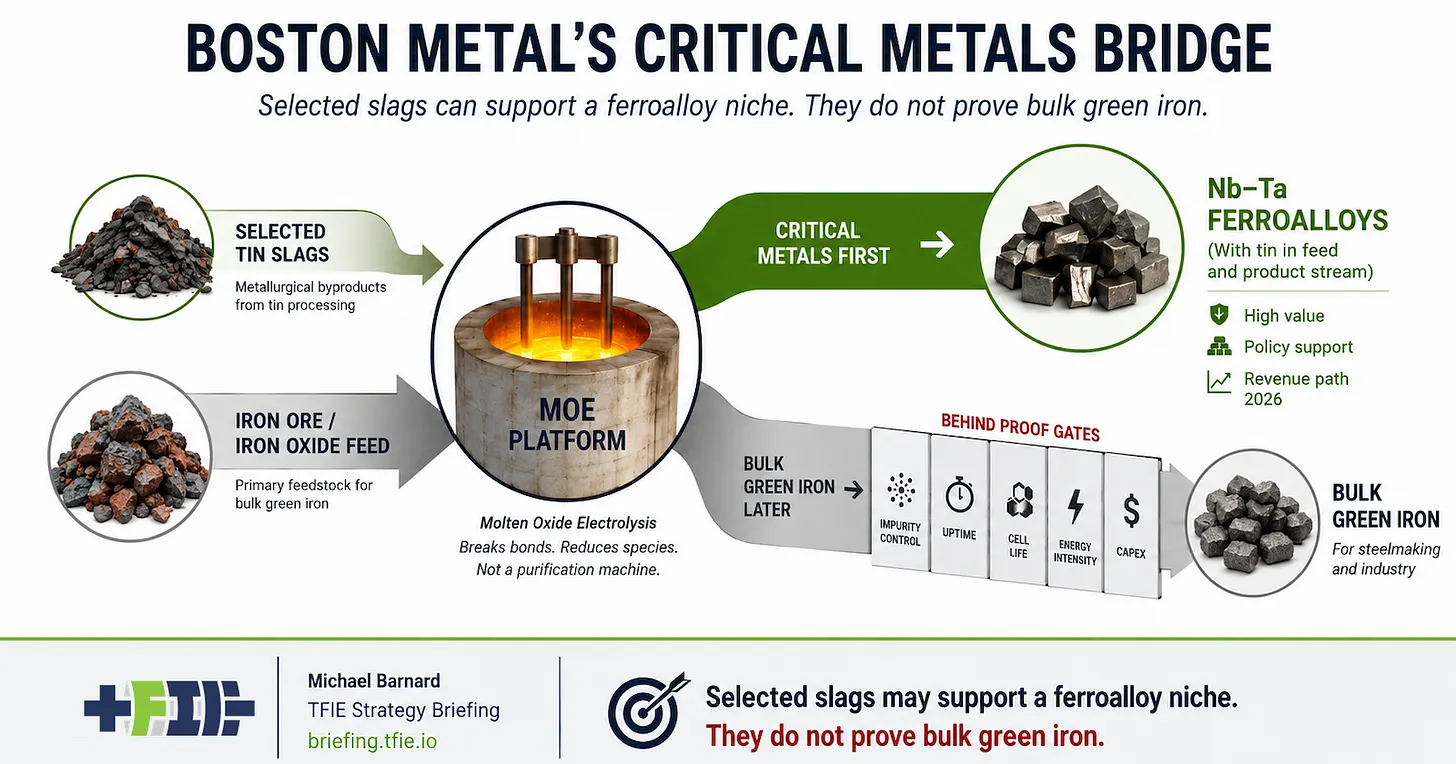

But the public evidence described in the latest analysis now points somewhere narrower and, in the near term, more commercially plausible. Rather than proving that bulk green iron is ready for industrial deployment, Boston Metal’s public direction increasingly supports a case for recovering selected critical metals from suitable slag streams. That is a meaningful shift because the company’s reputation has largely been built on the promise of green steel.

The distinction matters. Making primary iron for steel is among the harshest commercial tests in manufacturing. A process cannot simply work in a laboratory cell or pilot environment. It must run at enormous scale, maintain high uptime, survive long campaigns, handle variable feedstocks, protect refractory systems, manage anodes, achieve competitive energy intensity, and fit into a commodity market with punishing cost expectations. In that environment, technical elegance is not enough.

Why critical metals may be the more credible first market

The critical-metals pathway described in the source material changes the burden of proof. Instead of immediately displacing conventional ironmaking, Boston Metal appears more clearly aimed at processing selected tin slags into ferroalloys involving niobium, tantalum, and tin. That is a smaller and less sweeping opportunity than decarbonizing steel, but it is also easier to understand as a first commercial target.

Specialty and critical metals can tolerate higher process costs than commodity iron. If a slag stream is sufficiently enriched, the recovered value may justify additional processing steps that would be uneconomic in bulk steel production. In other words, the economics are different. A process that would struggle to compete ton-for-ton against incumbent ironmaking may still have a rational place in a more selective, higher-value materials market.

That does not make the challenge trivial. The source text is explicit that many “metals from waste” narratives break down when the gap between contained value and recoverable margin becomes clear. Even if the chemistry works, the real commercial questions remain stubbornly practical: recovery rates, energy use, impurity control, product quality, maintenance burden, campaign length, residue handling, and whether customers will qualify the output for real supply chains.

This is a useful reframing. It does not diminish the importance of molten oxide electrolysis. It changes what observers should ask of it right now. For critical-metals recovery, the relevant question is not whether the technology can one day transform all primary steelmaking. It is whether it can deliver repeatable, bankable performance on a narrower class of feedstocks where the economics are more forgiving.

Green iron still faces a separate proof burden

The analysis does not argue that Boston Metal’s original steel ambition is impossible. It argues that the evidence currently available does not yet prove the commercial case for green iron. That is a more disciplined conclusion than either dismissing the technology outright or treating it as already validated.

Steel is a scale business above all else. Any contender in primary iron must show that it can behave like ordinary industrial plant, not an impressive experiment. That means durable hardware, stable operations, and costs that work inside a market defined by massive volumes and relentless price pressure. A process can reduce oxides successfully in principle and still fail as a steel business if maintenance is too high, cell life is too short, or energy demand is too expensive.

The source text underscores this gap by separating “the cell” from “the refinery.” Reducing species in a melt is only part of the story. Real operations must control what else reduces alongside target metals, especially when impurities are present. Feedstock composition and operating conditions can determine whether the output is commercially useful or merely chemically interesting. In steel, that tolerance for process instability is exceptionally low.

That is why the current evidence points more convincingly toward critical-metals recovery. A narrower application gives Boston Metal a more realistic venue to prove that molten oxide electrolysis can function reliably under industrial conditions and create durable economic value.

What the shift means for climate and industry

For climate watchers, the change may feel like a retreat from a grander vision. But it may also be the opposite: a sign of a company moving toward a more testable market rather than overstating readiness in one of the hardest sectors to disrupt. In industrial technology, credibility often improves when claims become more specific.

If Boston Metal can show that its process works commercially in selected critical-metals applications, that would still matter. It would validate parts of the operating model, build experience with harsh electrochemical systems, and provide real-world data on campaign life, maintenance, energy intensity, and materials handling. Those are not side issues. They are the foundation of whether a broader metals platform can ever scale.

It would also align with current strategic pressures. Governments and manufacturers increasingly care not only about decarbonization, but also about resilience in critical-minerals supply chains. Processes capable of recovering niobium, tantalum, tin, or related materials from industrial residues could gain attention if they reduce waste and create alternative supply sources.

Still, the source material does not support sweeping conclusions beyond that. The present case is one of directional credibility, not full validation. Public evidence suggests Boston Metal’s nearer-term opportunity is more likely to emerge in selected critical-metals recovery than in bulk green steel. That is a smaller story than the one many observers may have expected, but it is also a more concrete one.

In practical terms, that is where the company’s technology now appears easiest to judge. If molten oxide electrolysis can turn enriched slags into saleable ferroalloys with acceptable recovery, quality, and operating costs, Boston Metal will have demonstrated something important. If not, the steel narrative becomes even harder to sustain. For now, the evidence points to a company whose immediate commercial test is no longer whether it can remake ironmaking, but whether it can first prove itself in the more selective, higher-value world of critical metals.

This article is based on reporting by CleanTechnica. Read the original article.

Originally published on cleantechnica.com