Distributed solar ended 2025 on a high note

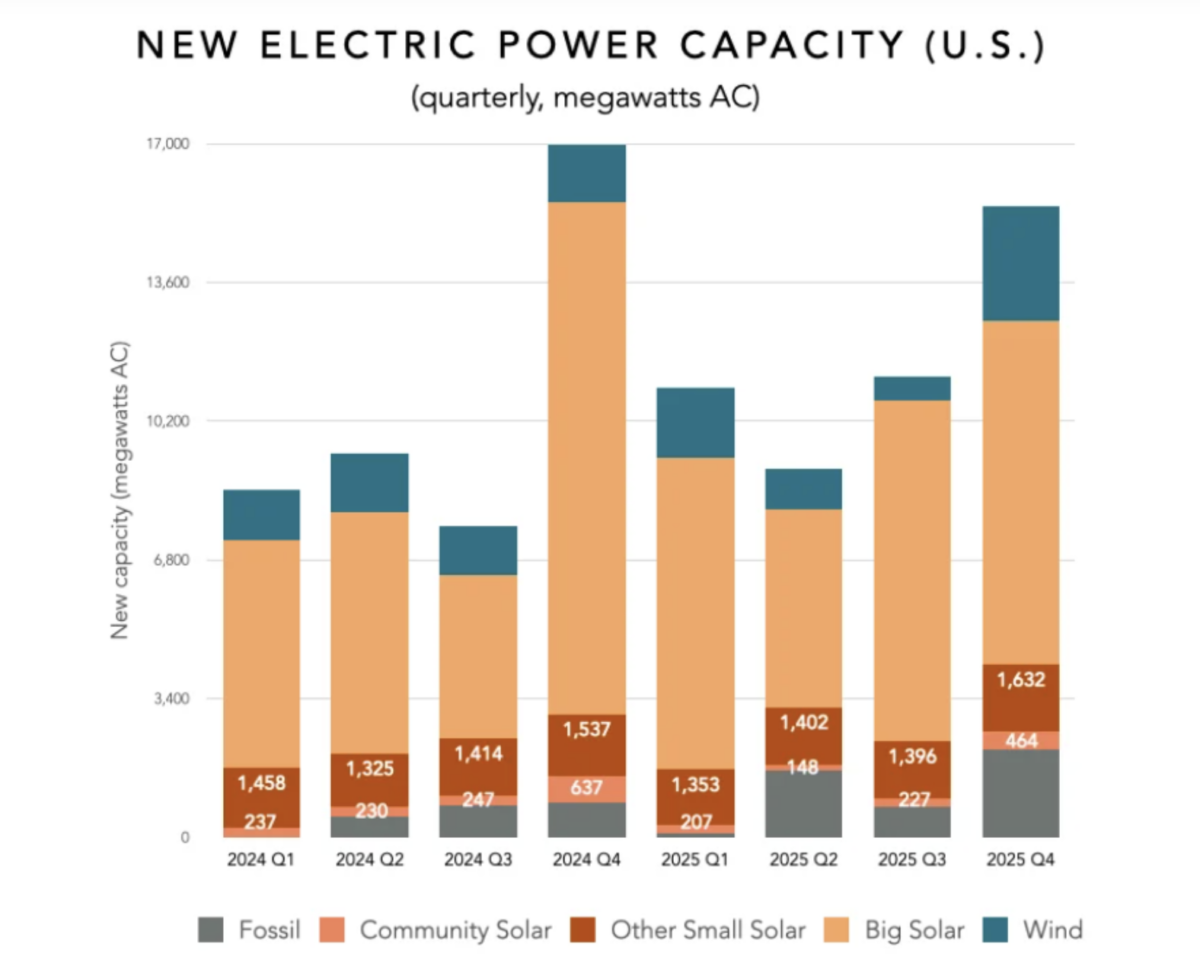

The U.S. small-scale solar market posted a record 1.9 gigawatts of new capacity in the fourth quarter of 2025, according to data cited by the Institute for Local Self-Reliance and the Energy Information Administration. The result marked a new quarterly high for distributed solar and closed out a year in which solar power broadly dominated new generating capacity added to the national grid.

The headline number matters because it shows that growth in U.S. solar is not being driven only by giant utility projects. Utility-scale plants still accounted for the largest share of installations, but residential and community systems made up a meaningful slice of the market. In 2025, distributed solar represented 15% of all new U.S. power capacity, a notable share for projects that are typically smaller than 1 megawatt and often connected behind the meter.

That distinction is important. Small-scale systems are usually installed on homes, businesses, schools, and community sites, which means they change the structure of the power system as much as they add raw capacity. Instead of concentrating generation at large remote plants, they spread electricity production closer to where it is consumed. That can help reduce strain on local grids, improve resilience in some areas, and broaden participation in the energy transition.

A record quarter capped a solar-heavy year

The fourth-quarter surge landed in a year when solar accounted for 78% of the 46 gigawatts of new power capacity added in the United States. That figure underscores how decisively solar has moved into the center of the country’s power buildout. Even with strong utility-scale momentum, the performance of distributed projects shows that households and communities are still responding to favorable economics and policy signals.

One factor identified by market analysts was a rush to secure the federal 25D residential energy efficient property tax credit. The source report says the incentive provided a 30% credit for solar electric property, and that the approach of policy deadlines helped push installations higher. If that interpretation is correct, the quarter was shaped not only by underlying demand for rooftop and community solar, but by the timing pressures that often come with tax incentives.

Such policy-driven acceleration is common in energy markets. Developers, homeowners, and installers frequently move projects forward when a credit or subsidy appears likely to change. In practice, that can make quarterly results look unusually strong even if the broader trend is one of steadier expansion. Still, the fact that distributed solar was able to produce a record quarter at all suggests the segment has achieved substantial scale.

Why distributed solar matters beyond the numbers

Distributed solar carries a different strategic value than utility-scale generation. Large solar farms are central to rapidly adding capacity at scale, but small systems can widen access to clean electricity and diversify ownership of energy assets. Community solar in particular can extend participation to customers who cannot install rooftop panels, including renters and households with unsuitable roofs.

The 2025 numbers also point to a more mature market. For years, distributed solar growth was closely associated with early-adopter states and high retail electricity prices. A record national quarter suggests broader demand patterns and improving deployment channels, even as financing conditions and policy uncertainty remain important constraints.

Because these systems are dispersed, they also interact with utility planning in more complicated ways than central-station power plants. High levels of behind-the-meter solar can reduce daytime demand on the grid, alter distribution system flows, and increase interest in complementary technologies such as batteries and demand management. Growth in small-scale solar therefore has implications far beyond installation totals.

Signals for 2026

The final-quarter record sets a strong benchmark heading into 2026, but it does not guarantee that the same pace will continue. If installations were pulled forward by tax-credit timing, some moderation could follow. At the same time, the annual numbers show that distributed solar is no longer a niche contributor. Even in a market led by big utility projects, residential and community systems are large enough to shape national capacity trends.

That leaves policymakers and utilities with a dual challenge. They must continue integrating large volumes of utility-scale solar while also adapting regulations, interconnection practices, and rate structures for a power system with far more customer-sited generation. The record quarter suggests that this is no longer a future problem. It is a current market reality.

What stood out in the data

- Small-scale U.S. solar installations reached 1.9 gigawatts in the fourth quarter of 2025.

- Solar accounted for 78% of the 46 gigawatts of new U.S. power capacity added in 2025.

- Residential and community solar contributed 15% of all new national power capacity.

- Analysts cited a rush to secure the 25D residential tax credit as one likely driver of late-year demand.

The broader takeaway is straightforward: distributed solar remains a meaningful growth engine inside the larger American solar market. Utility-scale projects may dominate the headline totals, but the record quarter shows that local, customer-connected solar is still expanding fast enough to matter nationally.

This article is based on reporting by PV Magazine. Read the original article.

Originally published on pv-magazine.com