South Australia expands its renewable buildout map

South Australia has opened more than 11,000 square kilometers of land for potential renewable energy development, marking another policy step in the state’s push toward a 100% net renewables target by 2027. The newly released areas are being offered through feasibility licenses under the state’s Hydrogen and Renewable Energy Act, with officials inviting proposals for large-scale solar, wind, and energy storage projects.

The move is notable not just for the size of the land release, but for what it signals about how the state is trying to organize its next phase of buildout. Rather than waiting for projects to emerge piecemeal, the government is defining specific zones and seeking investor interest in places already identified as having strong renewable potential. That creates a more structured pathway for developers and gives policymakers a clearer way to align generation, storage, and industrial planning.

Two zones, one broader strategy

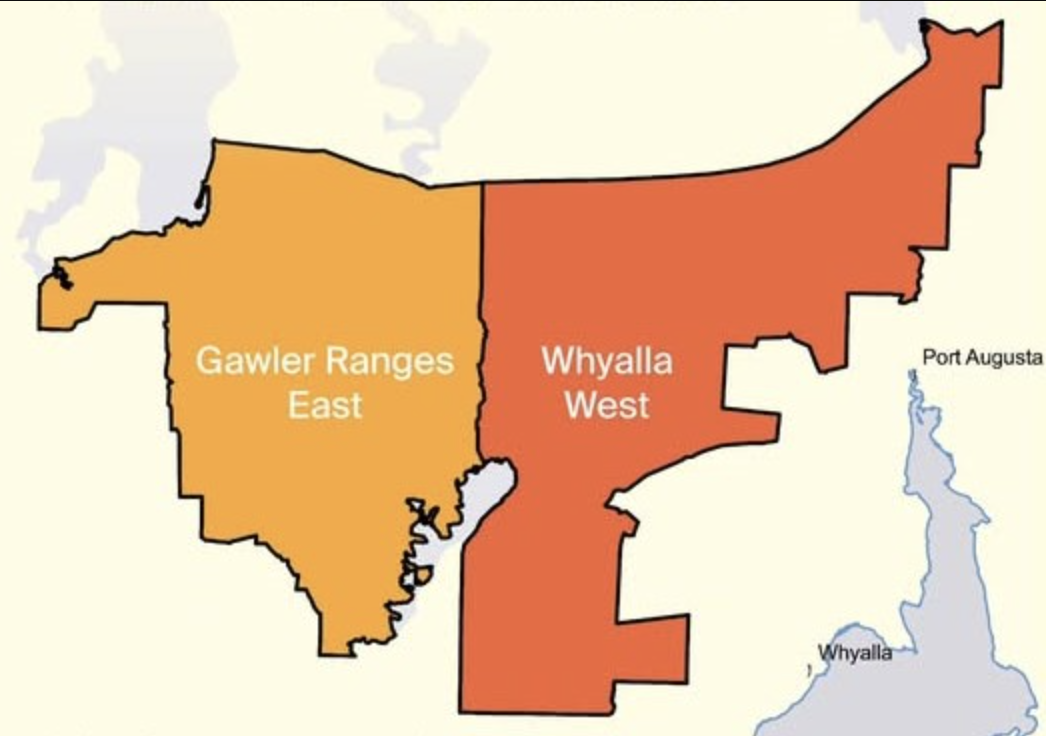

The two areas now open are Whyalla West and Gawler Ranges East. Together they span more than 11,000 square kilometers. According to South Australia’s Department of Energy and Mining, Gawler Ranges East covers roughly 5,200 square kilometers on the Upper Eyre Peninsula, while Whyalla West covers about 6,500 square kilometers in the Upper Spencer Gulf region.

Those locations were not selected at random. The department said the sites include some of the highest co-incident wind and solar resources in the state. In practical terms, that matters because projects in such areas can make better use of shared infrastructure and can produce more balanced renewable output across different weather conditions.

The state says the two release areas could host projects capable of powering more than 500,000 homes. That figure is an estimate rather than a build commitment, but it gives a sense of the scale being contemplated. It also underlines how South Australia continues to think beyond isolated installations and toward region-shaping energy clusters.

Why feasibility licenses matter

The immediate opening is for feasibility licenses, not full project approvals. That distinction is important. A feasibility license gives developers the right to investigate whether a project can work in a given area, including technical, environmental, commercial, and planning considerations. It is an early-stage gate that can determine whether a concept moves forward at all.

For governments, this approach helps narrow the field before larger commitments are made. For developers, it creates a formal route to test a project’s viability in territory already recognized by the state as strategically important. In effect, it reduces some of the uncertainty that can slow large renewable projects before construction decisions are reached.

By opening applications globally, South Australia is also signaling that it wants competition and outside capital. That matches the broader pattern in renewable energy markets, where jurisdictions increasingly compete not only on resource quality but on the clarity of their regulatory process.

A state already deep into the transition

South Australia has long been one of Australia’s most aggressive renewable energy markets, and this latest land release fits that identity. The state’s 2027 goal of reaching 100% net renewables gives the policy immediate relevance: this is not a distant roadmap item but part of a near-term race to secure enough generation and storage capacity to support the target.

The emphasis on solar, wind, and storage together is especially telling. Storage is no longer an optional add-on in large renewable planning. It is increasingly central to how governments and developers frame grid reliability, dispatchability, and the ability to absorb more variable generation. A release process that explicitly includes storage reflects how the market has changed.

The use of the Hydrogen and Renewable Energy Act also points to a wider industrial logic. Renewable zones can support not only electricity supply but also future hydrogen-linked activity, energy-intensive processing, and broader regional development. The policy vehicle itself suggests that South Australia is treating renewable deployment as an economic development strategy as much as a decarbonization exercise.

Why this announcement matters beyond the state

Large land releases do not guarantee projects will be built, and feasibility work can still expose grid, environmental, financing, or community constraints. Even so, the announcement is significant because it shows one way governments are trying to keep renewable momentum moving: define the geography, publish the framework, and invite developers into a more organized process.

That matters in a market where delays often have less to do with technology than with siting, permitting, and infrastructure coordination. South Australia’s release offers a case study in trying to get ahead of those bottlenecks by planning the pipeline before projects are locked in.

It also underscores a broader reality in the global energy transition. The next phase is not only about adding more megawatts. It is about finding the right places for those megawatts, aligning them with storage, and making the development path legible enough that capital will move. South Australia is betting that clearly designated renewable areas can help do exactly that.

If investor interest is strong, the result could be a new wave of utility-scale projects in some of the state’s best resource regions. If not, the release will still have served as a test of how much appetite exists for large, policy-led renewable expansion under a structured land access model. Either way, the state is pushing the market to answer an increasingly urgent question: how quickly can ambition be converted into buildable projects?

This article is based on reporting by PV Magazine. Read the original article.

Originally published on pv-magazine.com