More Solar, Lower Market Value

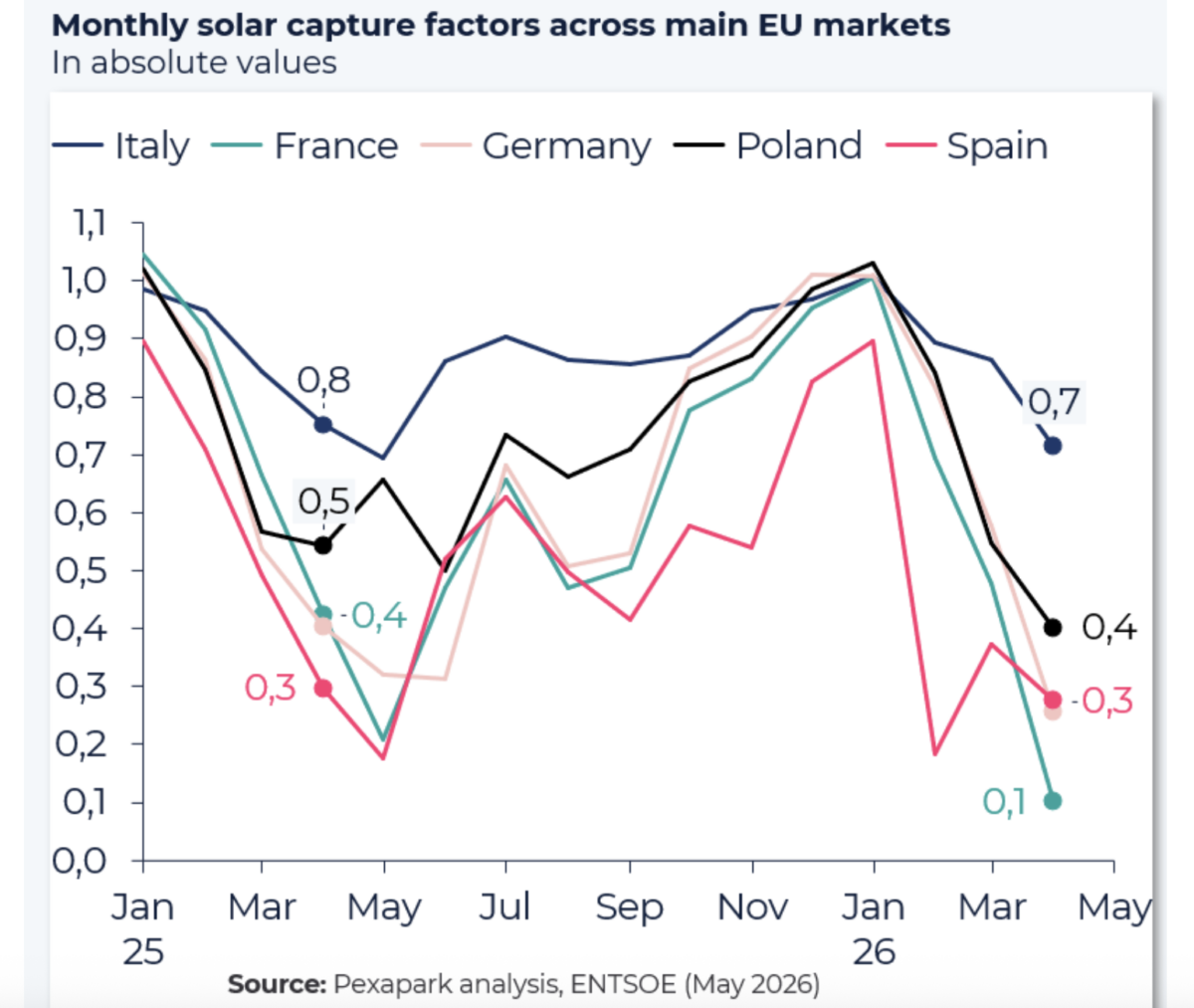

Europe’s solar sector is running into a problem that comes with success. New analysis from Swiss renewables research firm Pexapark shows that solar capture factors fell across several major power markets in April 2026, while the share of solar generation exposed to negative price hours increased. The pattern points to a structural challenge for power systems absorbing rapidly growing volumes of photovoltaic output: solar can keep producing more electricity even as the market pays less for it.

The decline was observed in France, Germany, Italy, Poland, and Spain. According to the analysis summarized in the source material, the drop happened despite broader commodity-market volatility linked to the Iran conflict. Pexapark analyst David Battista said that indicates the main driver is not fuel or geopolitics but structural oversupply dynamics inside Europe’s electricity system.

That distinction matters. If falling solar capture rates were mainly a temporary reaction to external shocks, the pressure might ease as those shocks faded. But if the trend is rooted in the way European markets are now balancing generation and demand, it points to a more durable economic issue for project owners, traders, and policymakers.

What Capture Factors Reveal

A solar capture factor measures how the achieved market price for solar generation compares with the average wholesale power price. When capture factors fall, solar producers are effectively receiving a smaller share of the market value than the headline power price might suggest. This often happens because solar generation is highly concentrated in the same daylight hours, which can flood the system with supply and push prices down precisely when solar plants are producing most.

Pexapark’s latest comparison between April 2025 and April 2026 showed that this dynamic intensified in major European markets. France recorded the sharpest decline, and the same overall direction was visible in Germany, Italy, Poland, and Spain. At the same time, a larger proportion of solar output in these countries was generated during hours when prices turned negative.

Negative pricing is no longer an oddity in European power markets. It is becoming a recurring feature of systems with fast-growing renewable capacity but insufficient flexibility to shift demand, store surplus electricity, or move power efficiently across regions. For solar developers, that means the challenge is no longer only building generation. It is preserving revenue quality in a market increasingly saturated during peak solar hours.

Why This Is Happening Now

The core pattern described by Pexapark is straightforward: strong solar output met weaker demand, causing capture factors to deteriorate. That combination is especially potent in spring, when weather conditions can be favorable for photovoltaic generation while heating demand recedes and cooling demand has not yet peaked. The result is a mismatch between when electricity is abundant and when the system values it most.

As installed solar capacity rises, the mismatch can become self-reinforcing. Every additional solar plant adds low-marginal-cost generation during similar hours, increasing the likelihood that midday prices will be compressed or turn negative. That does not make solar less useful from an energy-security or decarbonization perspective, but it does change the economics of merchant exposure and long-term power-price assumptions.

The analysis suggests that this structural issue is now prominent across multiple markets rather than isolated to one or two heavily built-out systems. That regional breadth is important because it implies that the challenge is not simply local congestion or one-off weather anomalies. It reflects the broader stage of Europe’s renewable transition.

What It Means for Investors and Power Markets

For asset owners and financiers, falling capture factors can erode project returns even if headline wholesale prices remain volatile or elevated at other times of day. A project may produce large volumes of electricity, yet earn less than expected because its output increasingly coincides with low-value or negative-value hours. That is a different risk from outright curtailment, but it can be just as consequential for revenue models.

The trend also places more weight on hedging strategies, storage integration, and contract design. Power purchase agreements, route-to-market structures, and co-located batteries become more important when raw generation growth no longer translates cleanly into proportional revenue growth. Developers who once focused primarily on irradiation and module costs are now forced to pay greater attention to cannibalization risk within their own technology class.

From a system perspective, the data strengthen the case for flexibility investments. Storage can shift excess midday supply into more valuable evening hours. Demand response can help align consumption with renewable abundance. Transmission improvements can move surplus power to regions where it is still needed. Market design can also influence how efficiently negative-price periods are handled and how flexible resources are rewarded.

A Sign of Maturity, Not Failure

There is a temptation to read negative prices and weak capture factors as evidence that solar growth has gone too far. That would be the wrong conclusion. The more useful interpretation is that Europe’s power transition is entering a more mature phase, where success in deployment must be matched by success in integration.

Solar oversupply during certain hours is, in one sense, a desirable problem compared with fossil-fuel scarcity. But it is still a problem. If renewable assets cannot earn sustainable returns, future investment can slow. If grids and markets cannot absorb variable generation efficiently, decarbonization becomes more expensive than necessary. The issue is no longer whether solar can scale. It is whether the rest of the system can keep pace.

Pexapark’s analysis underscores that this is already a commercial reality, not a distant theoretical concern. The drop in capture factors across France, Germany, Italy, Poland, and Spain shows that market value compression is spreading through Europe’s biggest solar economies. Rising exposure to negative-price hours makes the signal even clearer.

The implication for policy and industry is not to build less solar, but to build the complementary infrastructure and market tools that let high-solar systems function well. Storage, flexible demand, better interconnection, and smarter commercial structuring are moving from optional enhancements to central requirements.

Europe’s solar fleet is producing exactly the kind of clean electricity the energy transition demands. The next challenge is ensuring that markets know what to do with so much of it, all at once.

This article is based on reporting by PV Magazine. Read the original article.

Originally published on pv-magazine.com