A $4.75 Billion Bet on Clean Power

Google has acquired Intersect Power, one of the United States' fastest-growing renewable energy developers, in a transaction valued at approximately $4.75 billion including assumed debt. The deal, reported by Greenbelt Capital Partners, represents one of the largest direct acquisitions of a renewable energy company by a major technology firm and underscores the extent to which AI's energy demands are reshaping corporate strategy at the highest levels.

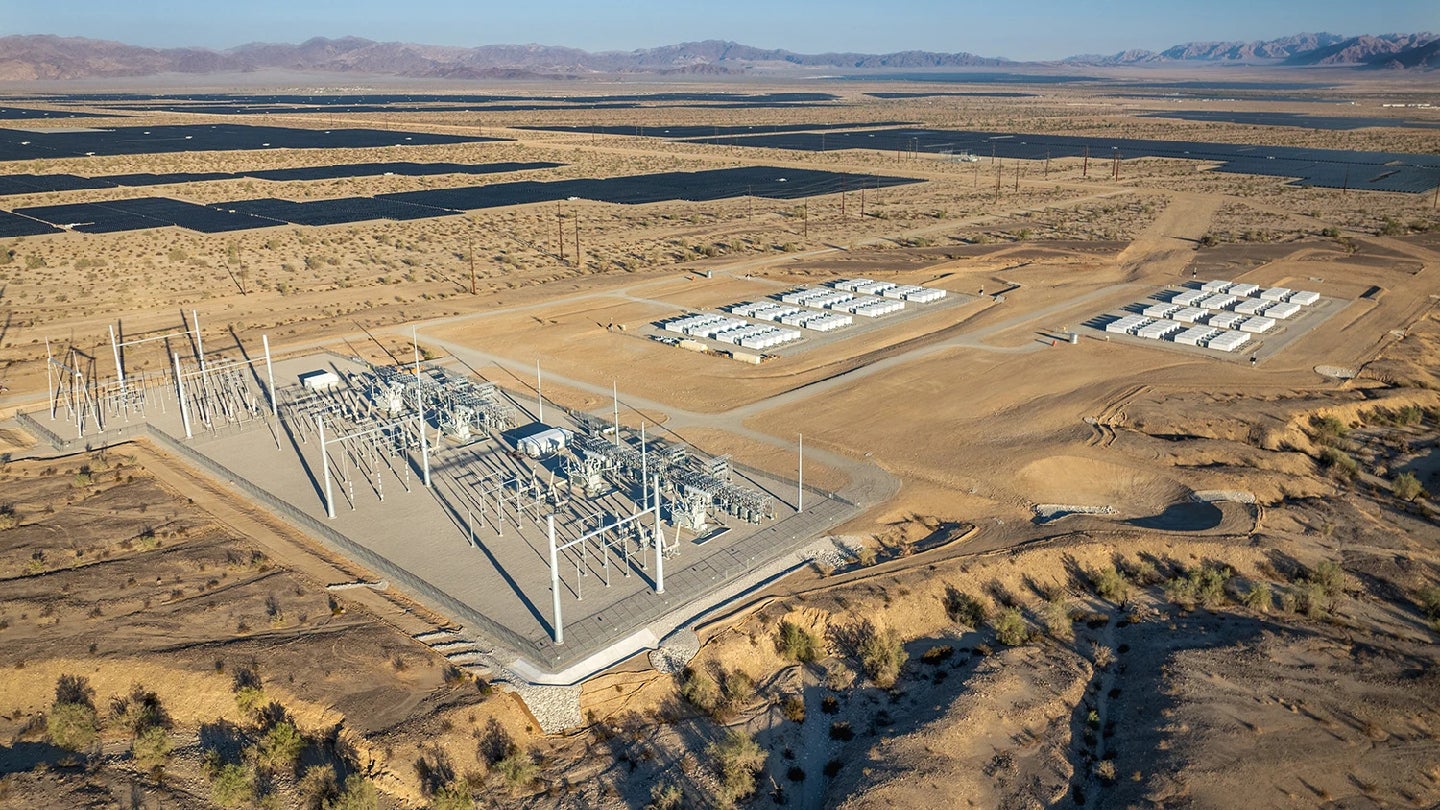

Intersect Power had built a portfolio of utility-scale solar and battery storage projects concentrated in the American West and Southwest—prime locations for solar irradiance and close to major population centers that require reliable power. The company had developed a reputation for speed and efficiency in project development, moving from site control to operational capacity faster than many larger competitors.

Why This Deal, Why Now

The timing reflects a convergence of pressures that has been building for several years. Google's AI infrastructure requires enormous amounts of electricity. Training large language models can consume the energy equivalent of thousands of homes over weeks of continuous computation. Inference—running those models to answer user queries—is even more energy-intensive in aggregate because it happens continuously at massive scale.

At the same time, Google has made public commitments to operate on 24/7 carbon-free energy by 2030—meaning it needs clean power available around the clock, not just on average. That requires a combination of solar, wind, geothermal, and storage assets that can cover periods when solar and wind are not producing. Acquiring Intersect Power gives Google direct ownership of assets rather than reliance on power purchase agreements, which are more flexible but less strategic.

The AI Data Center Arms Race

Google is not alone in this calculation. Microsoft has signed agreements to restart the Three Mile Island nuclear plant. Amazon has made investments in nuclear and geothermal projects. Meta has announced plans for dedicated power generation facilities adjacent to its data centers. The technology sector is collectively adding demand to power grids at a pace that utilities and regulators are struggling to plan around.

Acquiring an independent power developer rather than simply buying electricity from the grid gives Google several advantages. It removes a layer of counterparty risk. It allows Google to direct where projects are built—aligning generation with data center locations. And it gives Google a development pipeline it can accelerate or pause based on its own infrastructure plans rather than a third party's schedule.

Intersect Power's Portfolio and Pipeline

Intersect Power had a substantial operational portfolio at the time of acquisition, with additional gigawatts in various stages of development. The company had specialized in co-locating solar generation with battery storage, a combination that addresses one of renewable energy's core weaknesses—the mismatch between when the sun shines and when power demand peaks.

The company also had early-stage exploration of hydrogen production from renewable electricity, a technology that could eventually allow Google to store excess renewable energy in chemical form rather than losing it to grid curtailment. That optionality likely contributed to the acquisition valuation.

Regulatory and Policy Context

The acquisition comes as the US government is actively competing with itself on energy policy. The Inflation Reduction Act created substantial incentives for clean energy development that made projects like Intersect Power's financially attractive. At the same time, proposed regulatory changes and tariffs on solar components from some manufacturing regions created uncertainty about project costs.

By internalizing the development function, Google can more nimbly manage these policy risks. If incentive structures change, an internal development organization can pivot faster than a contractual relationship with an external developer.

Implications for the Energy Sector

The deal signals that major technology companies may increasingly acquire rather than contract for clean energy. For independent renewable developers, this trend creates both opportunity—the prospect of acquisition premiums—and risk, as technology companies with deep capital may outcompete them for project sites and grid interconnection queues.

Utility companies that have long positioned themselves as the natural owners of large-scale generation assets may find that the largest electricity consumers are choosing vertical integration instead. That shift has significant implications for how the energy sector is structured over the coming decade.

This article is based on reporting by Energy Monitor. Read the original article.

Originally published on energymonitor.ai