The Manufacturing Case for SMRs Is Running Into a Scale Problem

Small modular reactors have long been sold as nuclear power’s pragmatic reboot: smaller units, factory production, lower capital at risk, and less exposure to the delays and overruns that have hurt large reactor projects. But a new critique argues that the sector’s core promise depends on one condition the industry still has not met: convergence.

According to the source material, the economic case for SMRs was never simply about making reactors smaller. It was about making the same or very similar reactors repeatedly, with stable tooling, stable suppliers, stable inspection regimes, stable training, and sustained demand. That is the industrial logic that drove cost declines in solar panels, batteries, and wind turbines. Repetition, not rhetoric, creates learning curves.

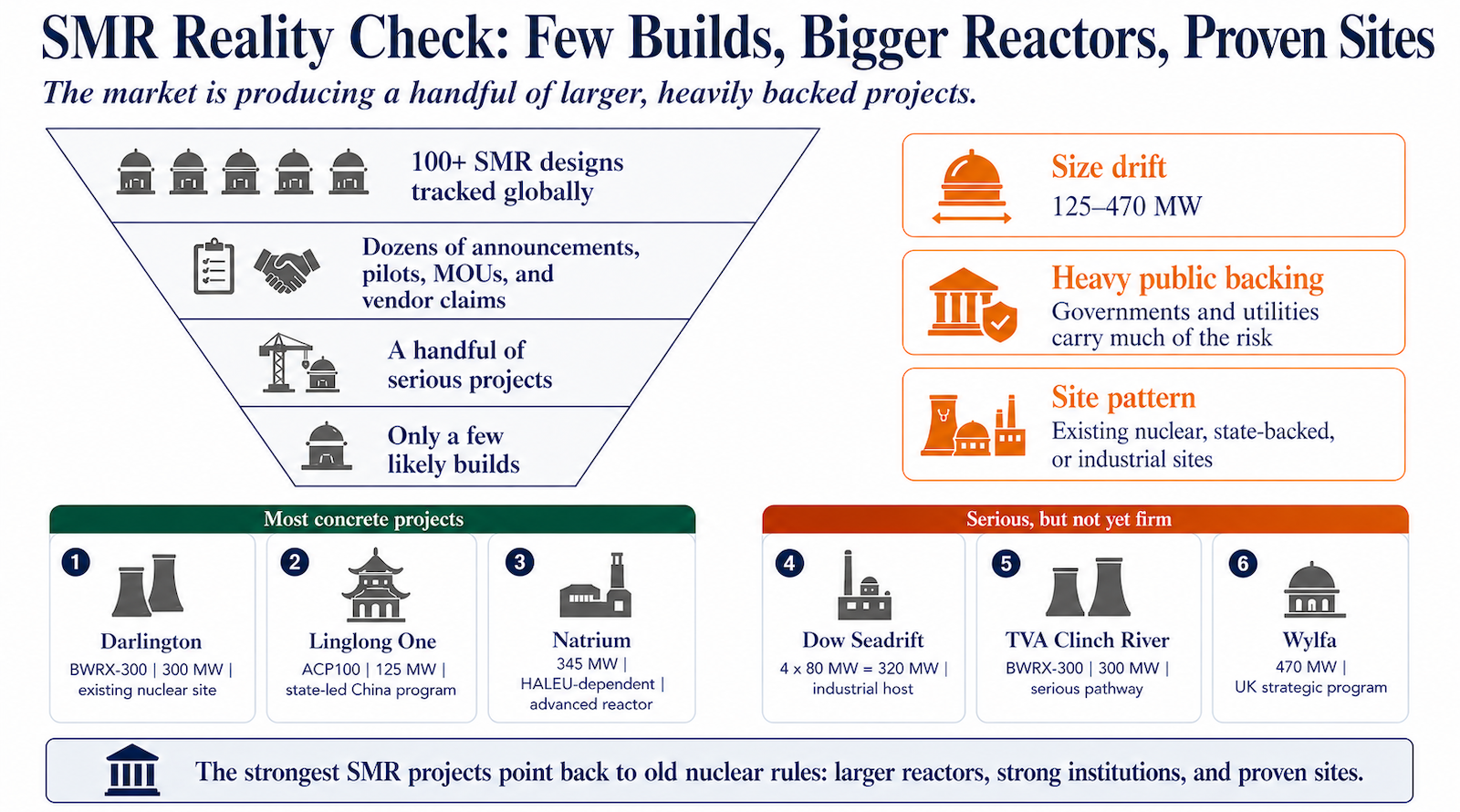

The problem for SMRs is that the field remains crowded with competing approaches. The source says an earlier assessment identified 57 SMR designs and concepts across 18 broad types. Since then, the OECD Nuclear Energy Agency’s dashboard has tracked more than 120 SMR technologies worldwide, with roughly 70 to 80 appearing in recent editions after excluding some paused, inactive, unfunded, or non-participating designs. Instead of narrowing toward a small set of dominant platforms, the landscape remains dispersed.

Why Fragmentation Matters

That fragmentation matters because nuclear projects are not interchangeable consumer products. Every design carries its own safety case, fuel qualification pathway, licensing process, site requirements, security arrangements, operator training needs, waste planning, and long-tail liability structure. In other words, the cost of variety is unusually high.

The source’s argument is straightforward: factory manufacturing does not create cost declines simply because it is invoked in presentations. Standardization is what allows a factory model to pay off. Without that, each design family risks becoming its own industrial island, too small to produce the manufacturing repetition needed to bring costs down.

This is a sharper version of a criticism that has followed SMRs for years. Proponents have correctly identified major weaknesses in large conventional nuclear builds. Large plants are expensive to finance, take years to complete, and can impose major balance-sheet and political risks if they fail. SMRs promise a way around those constraints. But if the trade-off is a global sector split among dozens of distinct concepts, the hoped-for advantages of modular production may be diluted before they are realized.

The Tension at the Center of the SMR Pitch

The source frames the original SMR proposition as elegant but fragile. Smaller reactors sound easier to permit, finance, deploy, and replicate. They also appear better suited to a wider range of sites. Yet the very diversity that has emerged around SMRs cuts against the discipline required for large-scale industrial learning.

That tension is now harder to ignore. The sector has not moved from a crowded field toward a clear set of winners. Instead, the dashboard counts cited in the source suggest that fragmentation remains a defining feature of the market. That does not mean SMRs cannot produce useful low-carbon electricity. The critique explicitly separates the value of nuclear generation from the policy case for backing a broad field of highly differentiated small-reactor designs.

The more important question is whether public policy and private investment are being aligned with the conditions under which nuclear power has historically scaled. The source’s answer is no. Scaling, in this view, requires discipline: fewer designs, more repetition, and a market structure capable of supporting continuous production of standardized units over time.

What This Means for Energy Policy

For governments, utilities, and investors, the warning is less about physics than industrial organization. A fragmented SMR market may generate engineering activity, pilot projects, and a constant stream of announcements without establishing the production base needed for broad cost reductions. That would leave the sector with many of the burdens of nuclear development but fewer of the benefits promised by modularity.

The article also arrives at a moment when energy planners are balancing multiple pressures at once: decarbonization, grid reliability, energy security, and financing discipline. In that context, technologies that depend on standardization need more than enthusiasm. They need a path to concentration. Without it, the sector risks becoming a showcase of promising exceptions rather than a repeatable industrial system.

That is the real challenge embedded in the SMR debate. The issue is not whether smaller reactors can be built. It is whether they can be built often enough, similarly enough, and predictably enough to validate the economic story that made them politically attractive in the first place.

This article is based on reporting by CleanTechnica. Read the original article.

Originally published on cleantechnica.com