Regulation Is No Longer the Bottleneck

The conversation around electric vertical takeoff and landing aircraft has shifted fundamentally. The FAA finalized powered lift operational rules in 2024 and published Advisory Circular 21.17-4 in 2025. The European Union Aviation Safety Agency published its Special Condition VTOL framework back in 2019 with subsequent guidance updates. The regulatory infrastructure for certifying eVTOL aircraft now exists on both sides of the Atlantic. The actual bottlenecks are engineering completion and financial endurance.

Using reference class forecasting that compares eVTOLs to historically novel aircraft categories like the AW609 tiltrotor, analyst Michael Barnard argues that 2027 certification is "statistically optimistic" and the more likely timeline points toward 2028. He assigns only a 20 to 30 percent probability to at least one firm achieving certification by 2027, with multiple certifications by that date falling below 15 percent.

The Cash Runway Problem

The financial picture for leading eVTOL companies is sobering. Archer reported $509.7 million in annual operating expenses for 2024, with Q3 spending up 43% year-over-year. Joby spent $535.4 million in the first nine months of 2025 compared to $447 million in the same period of 2024. BETA Technologies saw R&D costs rise 17% and administrative expenses jump 50% year-over-year. Late-stage aerospace certification typically doubles burn rates due to conforming aircraft builds, destructive testing, and production tooling.

Under a doubled-burn scenario, BETA holds the strongest position with approximately $1.7 billion in liquidity and a runway extending into mid-to-late 2028. Joby's $1.55 billion provides roughly 1.4 years, creating funding pressure by early-to-mid 2027. Archer's $1.64 billion yields about 1.6 years of runway with similar 2027 pressure. Vertical Aerospace, with only $110 million in cash, cannot survive without a major capital injection.

Unit Economics Challenge Profitability

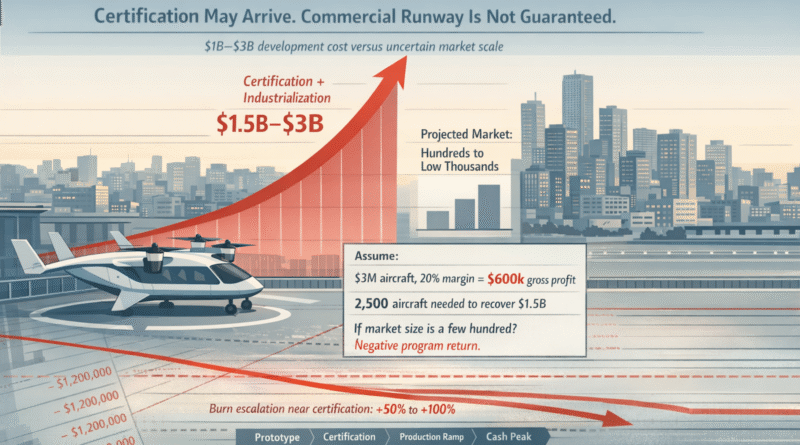

Even with certification in hand, profitability is far from guaranteed. At an estimated $3 million per aircraft with 20% gross margin, recovering $1.5 billion in development costs requires selling approximately 2,500 units. Market estimates suggest only low thousands of units globally over a full decade, with hundreds in early regional deployments. The FAA has also documented rotor-generated winds exceeding safety thresholds well beyond touchdown zones, requiring safety setbacks that reduce viable urban vertiport locations and limit operations per hour.

The Path Forward

For 2027 certification to occur, at least one company must have conforming aircraft in FAA or EASA testing by mid-2026, a stable configuration freeze, and sufficient liquidity to avoid emergency capital raises during the Type Inspection Authorization phase. BETA's CX300 derivative appears best positioned financially, while Joby and Archer are further along in powered lift certification but face burn-driven capital raise pressures. The determining factor is not whether eVTOLs can fly; it is whether their makers can survive long enough to prove it commercially.

This article is based on reporting by CleanTechnica. Read the original article.

Originally published on cleantechnica.com