कहानी उत्साह से अनुशासन की ओर बढ़ गई है

पिछले कुछ वर्षों में प्राकृतिक हाइड्रोजन ने स्वच्छ ऊर्जा में एक परिचित चक्र से गुज़राव किया है: शुरुआती आकर्षण, व्यापक दावे, और फिर भूविज्ञान, इंजीनियरिंग और अर्थशास्त्र की कठिन वास्तविकता से सामना। CleanTechnica का नवीनतम आकलन तर्क देता है कि यह क्षेत्र अब एक अधिक संयमित चरण में पहुँच गया है। प्राकृतिक रूप से पाए जाने वाले हाइड्रोजन का अस्तित्व अब मुख्य प्रश्न नहीं रहा। असली सवाल यह है कि क्या इतनी मात्रा में हाइड्रोजन खोजा, रोका, उत्पादित और बेचा जा सकता है कि वह एक टिकाऊ औद्योगिक व्यवसाय का आधार बन सके।

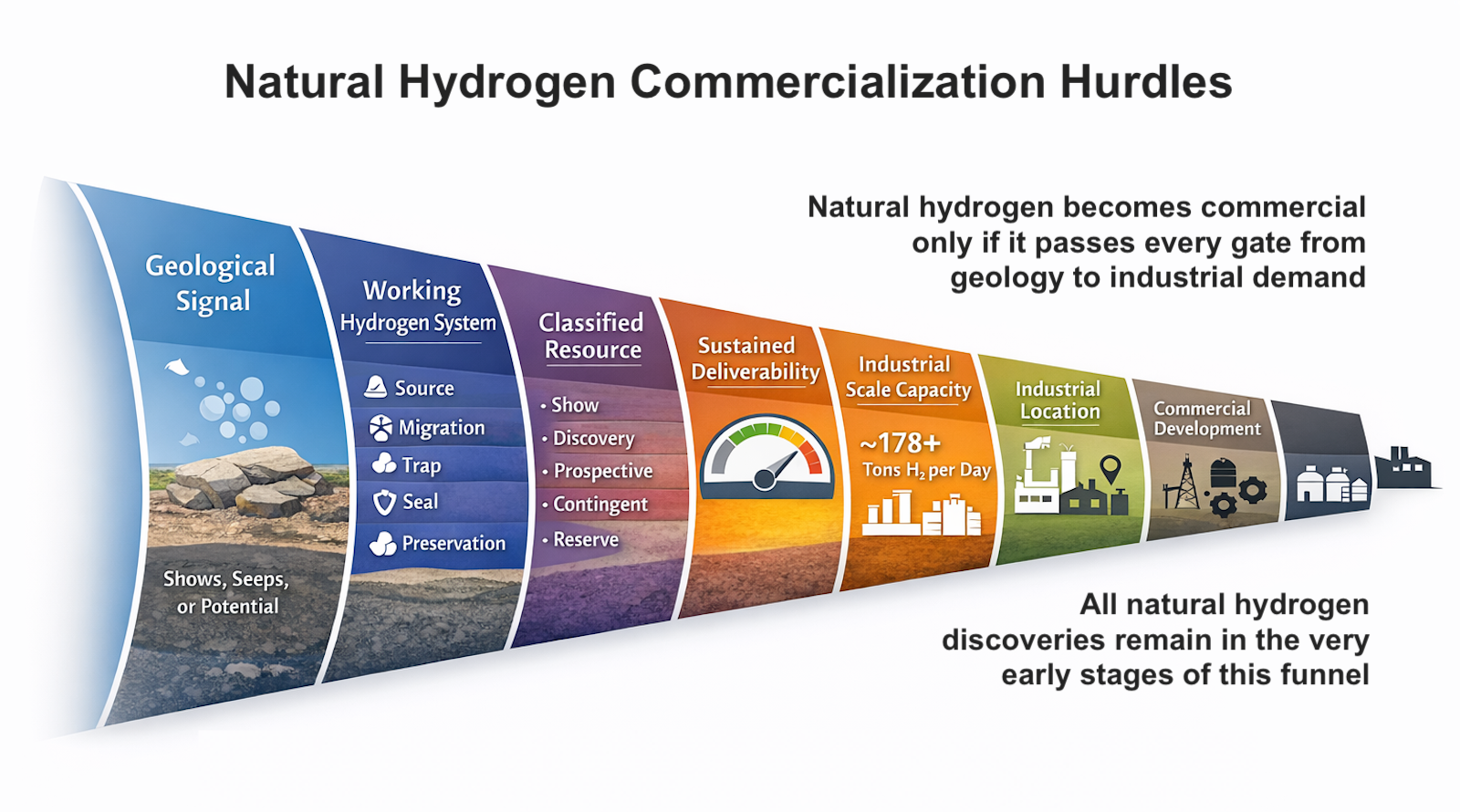

यह अंतर तकनीकी लग सकता है, लेकिन यही वैज्ञानिक जिज्ञासा और ऊर्जा उद्योग के बीच का फर्क है। कोई संसाधन ज़मीन के नीचे मौजूद हो सकता है, लेकिन व्यावसायिक रूप से महत्वपूर्ण नहीं बनता। लेख के अनुसार, समस्या यह नहीं है कि क्रस्ट में हाइड्रोजन बनता है या नहीं। समस्या यह है कि क्या कोई व्यवहार्य निष्कर्षण प्रणाली के लिए पूरी श्रृंखला दिखा सकता है: उत्पादन, प्रवासन, ट्रैपिंग, सीलिंग, संरक्षण और व्यावसायिक प्रवाह दरों पर आपूर्ति।

मौजूद होना भंडार के बराबर नहीं है

यहीं पर प्राकृतिक हाइड्रोजन को लेकर शुरुआती उत्साह अक्सर प्रमाण से आगे निकल गया। CleanTechnica का विश्लेषण हाइड्रोजन उत्पादन, हाइड्रोजन की उपस्थिति और हाइड्रोजन भंडार के बीच अंतर को रेखांकित करता है। भूवैज्ञानिक अब अधिक आश्वस्त हैं कि प्राकृतिक हाइड्रोजन serpentinization, radiolysis और iron oxidation जैसे तंत्रों से उत्पन्न हो सकता है। लेकिन उत्पादन से जमाव की गारंटी नहीं मिलती, और जमाव से व्यावसायिक रूप से निकाले जा सकने वाले क्षेत्र की गारंटी नहीं मिलती।

हाइड्रोजन अपने भौतिक व्यवहार के कारण विशेष रूप से चुनौतीपूर्ण मामला है। यह छोटा, प्रतिक्रियाशील और रिसाव-प्रवण होता है। यह सूक्ष्मजीवी गतिविधि या अजैविक प्रतिक्रियाओं से भी खो सकता है। इससे प्राकृतिक हाइड्रोजन, मीथेन की तुलना में, क्षेत्र विकास के दृष्टिकोण से कम क्षमाशील बन जाता है। कोई बेसिन हाइड्रोजन उत्पन्न कर सकता है, लेकिन उसे कभी उन सांद्रताओं, मात्राओं और आपूर्ति योग्यता में संरक्षित नहीं कर सकता जो औद्योगिक उपयोग के लिए चाहिए।

इसीलिए reserve भाषा महत्वपूर्ण है। तेल और गैस में, prospect reserve नहीं होता, और resource अपने-आप bankable asset नहीं बन जाता। लेख का तर्क है कि प्राकृतिक हाइड्रोजन को भी उन्हीं मानकों पर परखा जाना चाहिए। व्यापक रूप से घोषित reserve आँकड़े अभी भी दुर्लभ हैं, और माली फ़ील्ड जैसे benchmark स्थलों पर भी अभी तक वे सार्वजनिक रूप से सत्यापित reserve आँकड़े नहीं हैं जिनकी पारंपरिक ऊर्जा निवेशक सामान्यतः अपेक्षा करते हैं।

यह विफलता नहीं है, लेकिन यह वास्तविकता की जाँच है

महत्वपूर्ण बात यह है कि लेख इसे इस रूप में नहीं रखता कि यह क्षेत्र धोखाधड़ी है या doomed है। इसके उलट, यह इसे speculative headlines से “real extractive industry discipline” की ओर बढ़ते कदम के रूप में वर्णित करता है। कंपनियाँ prospective resources और appraisal जैसे शब्दों के उपयोग में अधिक सावधान हो रही हैं, जो बाज़ार के परिपक्व होने का संकेत है। लेकिन यहाँ maturity का मतलब अपेक्षाओं को बढ़ाना नहीं, उन्हें संकुचित करना है।

यह एक उपयोगी सुधार है। पहले के चरणों में प्राकृतिक हाइड्रोजन को कभी-कभी लगभग असीम स्वच्छ-ईंधन अर्थव्यवस्था की नींव की तरह चित्रित किया गया, मानो भूमिगत हाइड्रोजन का अस्तित्व ही आसान प्रचुरता सुनिश्चित कर देता हो। लेख में प्रस्तुत वर्तमान प्रमाण, कम-से-कम, एक अधिक सीमित दृष्टिकोण का समर्थन करते हैं। प्राकृतिक हाइड्रोजन कुछ चयनित संदर्भों में वास्तविक और मूल्यवान साबित हो सकता है, बिना उस व्यापक ऊर्जा क्रांति के जो कभी सुर्खियों में सुझाई गई थी।

वादा से प्रमाण तक का यह बदलाव क्षेत्र के लिए स्वस्थ है। हर गंभीर निष्कर्षण उद्योग अंततः reservoir quality, flow testing, development design, cost structure और commercial offtake पर लौटता है। प्राकृतिक हाइड्रोजन अब इसी कठिन चरण में प्रवेश कर रहा है। इससे यह कम दिलचस्प नहीं होता। इससे यह अधिक मापनीय हो जाता है।

यह क्षेत्र अभी भी ध्यान क्यों चाहता है

एक अधिक संशयात्मक ढाँचे के बावजूद, प्राकृतिक हाइड्रोजन महत्वपूर्ण बना हुआ है। यदि व्यावसायिक क्षेत्र साबित किए जा सकें, तो यह व्यापक हाइड्रोजन परिदृश्य में एक नया low-carbon या lower-carbon supply pathway जोड़ सकता है। यही संभावना बताती है कि यह क्षेत्र तकनीकी और निवेशक रुचि क्यों आकर्षित करता रहता है। लेकिन इसे परखने का सही तरीका अब केवल सैद्धांतिक वैश्विक abundance estimates नहीं रह गया है। इसे field-specific evidence से परखना होगा।

लेख का केंद्रीय तर्क है कि अब यही एकमात्र प्रश्न है जो मायने रखता है। यह नहीं कि हाइड्रोजन भूमिगत मौजूद है या नहीं, बल्कि यह कि क्या वह सही स्थान पर, सही दर पर और ऐसे हालात में मौजूद है जो दोहराए जा सकने वाले व्यावसायिक संचालन को सहारा दें। ये कठिन आवश्यकताएँ हैं, और कई संभावित परियोजनाएँ संभवतः इन्हें पूरा नहीं कर पाएँगी। संसाधन विकास में यह सामान्य है।

यही तर्क क्षेत्र को आत्म-क्षति से भी बचाता है। यदि कंपनियाँ और टिप्पणीकार दावे बढ़ा-चढ़ाकर पेश करते रहें, तो निराशाजनक कुएँ या कमजोर reserve disclosures अनावश्यक प्रतिकूल प्रतिक्रिया पैदा कर सकते हैं। एक अनुशासित मानक, भले कम रोमांचक हो, अंततः अधिक रचनात्मक है। यह क्षेत्र को hype नहीं, डेटा से मूल्य सिद्ध करने का मौका देता है।

छोटी संभावना भी संभावना है

व्यावहारिक निष्कर्ष यह नहीं है कि प्राकृतिक हाइड्रोजन को खारिज कर दिया जाए। निष्कर्ष यह है कि इसे किसी भी अन्य भूमिगत संसाधन व्यवसाय की तरह परखा जाए। appraisal wells, verified reserves, production testing और commercial integration ही इस क्षेत्र का भविष्य तय करेंगे। तब तक, आने वाले hydrogen bonanza के व्यापक दावे समय से पहले हैं।

यह उन लोगों को निराश कर सकता है जो किसी सरल स्वच्छ-ऊर्जा breakthrough की उम्मीद कर रहे थे। लेकिन credible industries भी इसी तरह बनती हैं। यदि प्राकृतिक हाइड्रोजन सफल होता है, तो वह इसलिए नहीं होगा कि उसने असाधारण अपेक्षाएँ पैदा कीं, बल्कि इसलिए कि कुछ परियोजनाएँ अंततः टिकाऊ reservoir behavior और commercial recovery दिखाएँगी। यदि यह विफल होता है, तो कारण यह नहीं होगा कि भूमिगत हाइड्रोजन काल्पनिक था; कारण यह होगा कि भूविज्ञान एक आर्थिक रूप से मज़बूत व्यवसाय में नहीं बदल पाया।

अभी के लिए, सबसे सटीक दृष्टि सबसे कम नाटकीय है: प्राकृतिक हाइड्रोजन वास्तविक है, दिलचस्प है, और संभावित रूप से उपयोगी है, लेकिन उसने अभी तक commercial scale पर proven energy solution का दर्जा हासिल नहीं किया है।

- प्राकृतिक हाइड्रोजन की भूवैज्ञानिक वास्तविकता अधिक स्पष्ट हो रही है, लेकिन व्यावसायिक भंडार अभी भी साबित नहीं हुए हैं।

- क्षेत्र के सामने अब flow rates, trapping और आर्थिक व्यवहार्यता दिखाने की कठिन चुनौती है।

- इसका भविष्य abundance narratives नहीं, बल्कि अनुशासित field evidence पर निर्भर करेगा।

यह लेख CleanTechnica की रिपोर्टिंग पर आधारित है। मूल लेख पढ़ें।

Originally published on cleantechnica.com