U.S. Automation Growth Returned in 2025

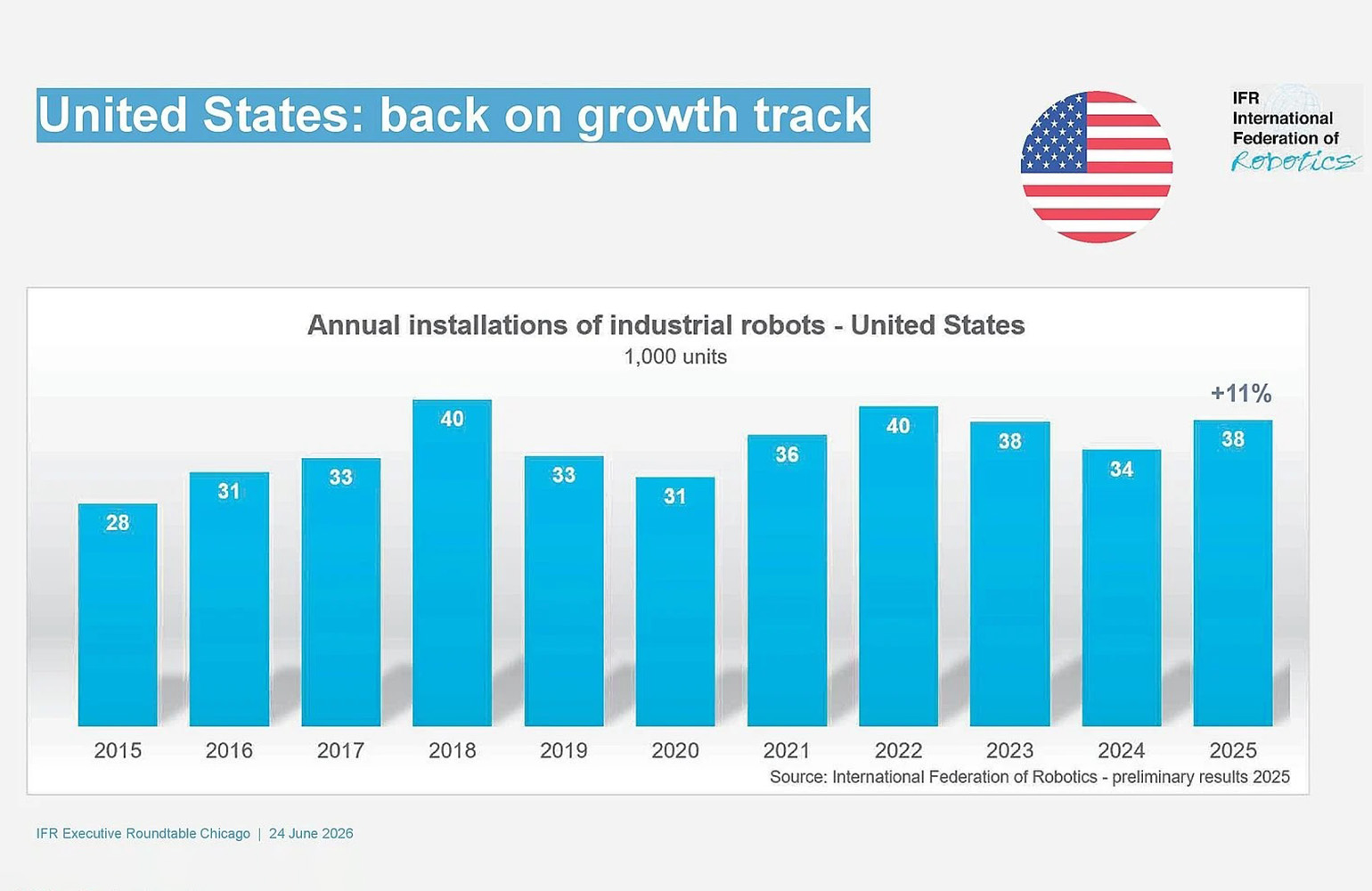

Industrial robot adoption in the United States grew at a double-digit pace in 2025, according to new figures from the International Federation of Robotics, offering a more upbeat reading on the country’s automation market after a period of uneven momentum. The IFR said U.S. installations reached 38,000 units last year, up 11% from 2024.

The headline matters not just because it signals recovery, but because of where the growth came from. Automotive manufacturing remained the country’s largest adopter of industrial robots, yet the strongest acceleration came from outside the sector. The IFR said robot installations in the food industry surged 30% in 2025, helping push the broader market higher and reinforcing a shift toward more diversified automation demand.

That is an important development for the shape of the U.S. robotics economy. For years, industrial robot adoption in America has been closely tied to automotive spending cycles. Those cycles still matter, but the latest figures suggest the market is widening, with non-manufacturing and non-automotive use cases becoming more meaningful contributors to growth.

Automotive Still Leads, but No Longer Tells the Whole Story

The automotive industry installed 13,500 units in 2025, just 1% below the previous year, according to the IFR. That level still made it the largest single adopter in the U.S. market and marked what IFR President Takayuki Ito described as the sector’s third-best result in seven years.

But the notable change is that other sectors are increasingly closing the gap in strategic significance. The IFR said food industry adoption climbed enough to place it alongside metal and machinery and electrical-electronics, with each segment posting roughly 3,000 installations in 2025. In other words, growth is no longer coming from one dominant industrial lane alone.

That matters for resilience. A robotics market tied too tightly to a single sector can rise and fall with a narrow band of capital expenditure decisions. A broader customer base means more stable demand, more experimentation across workflows, and a larger market for suppliers building flexible automation systems rather than highly specialized line equipment.

The IFR’s framing emphasizes exactly that point. The organization described the current trend as a growing appetite for flexible automation, especially in industries dealing with labor shortages, higher throughput demands, and mounting pressure to improve consistency and traceability.

Robot Density Shows Progress, but Also the Gap

The federation’s data also points to a second reality: even with stronger growth, the U.S. is still not the most automated industrial economy. The country’s robot density now stands at 307 industrial robots in operation for every 10,000 manufacturing employees, placing the United States eighth worldwide, up two places from the prior year.

That ranking shows real progress, but it also highlights the distance between the U.S. and the highest-density markets. South Korea leads with 1,220 robots per 10,000 employees, followed by Germany at 449 and Japan at 446, according to the IFR figures cited in the source text. China trails those leaders on density at 166, but density alone does not describe overall market scale.

On raw installations, China remains far ahead of every other country. The IFR said annual robot installations in China reached 295,000 units in 2024, equal to a 54% share of the global market. The organization had not yet published preliminary 2025 figures for China, but estimated the country’s annual installations were about ten times higher than those of the United States.

The Strategic Comparison With China

The U.S.-China comparison is unavoidable because it turns a market update into an industrial policy question. The IFR attributes China’s scale in part to a long-running national robotics strategy launched a decade ago. It also pointed to China’s newly published 15th Five-Year Plan for 2026 through 2030, which places robotics at the center of the country’s modern industrial system and links AI research to physical applications.

That claim is significant because it underscores how robotics is increasingly being treated as a national capability, not just a factory technology category. The countries that lead in automation are likely to gain advantages in output, supply chain resilience, workforce allocation, and commercialization of embodied AI. Industrial robots sit at the practical edge of those transitions because they translate software, sensing, and machine intelligence into physical work.

For the United States, the latest growth figures are encouraging, but they do not erase the scale disparity. A rebound to 38,000 annual installations shows renewed appetite. It does not yet establish dominance, nor does it fully answer whether U.S. policy and investment are aligned with long-term competitive needs.

Why the U.S. Outlook Remains Positive

The IFR’s outlook for North America remains optimistic. It cited factory reshoring initiatives and persistent shortages of skilled labor as structural drivers likely to support further investment in automation. Those factors are important because they are not temporary demand spikes. They are broad constraints that push manufacturers toward robotics even when economic conditions fluctuate.

Reshoring, in particular, changes the business case for automation. When companies bring production closer to home, they often face higher labor costs and tighter labor availability than in offshore manufacturing hubs. Robots can help close that gap by improving utilization, reducing repetitive manual tasks, and enabling production models that are more viable domestically.

Labor scarcity adds another layer. In many industries, the problem is not simply wage inflation; it is the difficulty of staffing repetitive or physically demanding roles consistently. That makes robotics less of an optional modernization project and more of a practical response to workforce constraints.

- U.S. robot installations rose 11% year over year to 38,000 units in 2025.

- Food industry adoption increased 30%, signaling broader demand beyond automotive.

- The U.S. ranks eighth globally in robot density, but remains far behind China in market size.

A Broader Shift in Industrial Technology

The 2025 numbers suggest the U.S. robotics sector is entering a more mature phase, one in which demand becomes less concentrated and more closely tied to structural pressures across the economy. That does not mean growth will be smooth. Capital spending cycles, interest rates, and sector-specific slowdowns will continue to shape annual totals.

Still, the latest IFR data points to a durable direction of travel. Automation is expanding into more corners of the U.S. economy, and the industries adopting robots are not doing so for novelty. They are doing it because throughput, labor availability, and competitiveness increasingly depend on it.

For investors, manufacturers, and policymakers, that makes this more than a statistical rebound. It is evidence that robotics in the United States is becoming a wider industrial shift rather than a narrow automotive story. The pace may not yet match the world’s largest markets, but the trajectory is clearer than it has been in years.

This article is based on reporting by The Robot Report. Read the original article.

Originally published on therobotreport.com