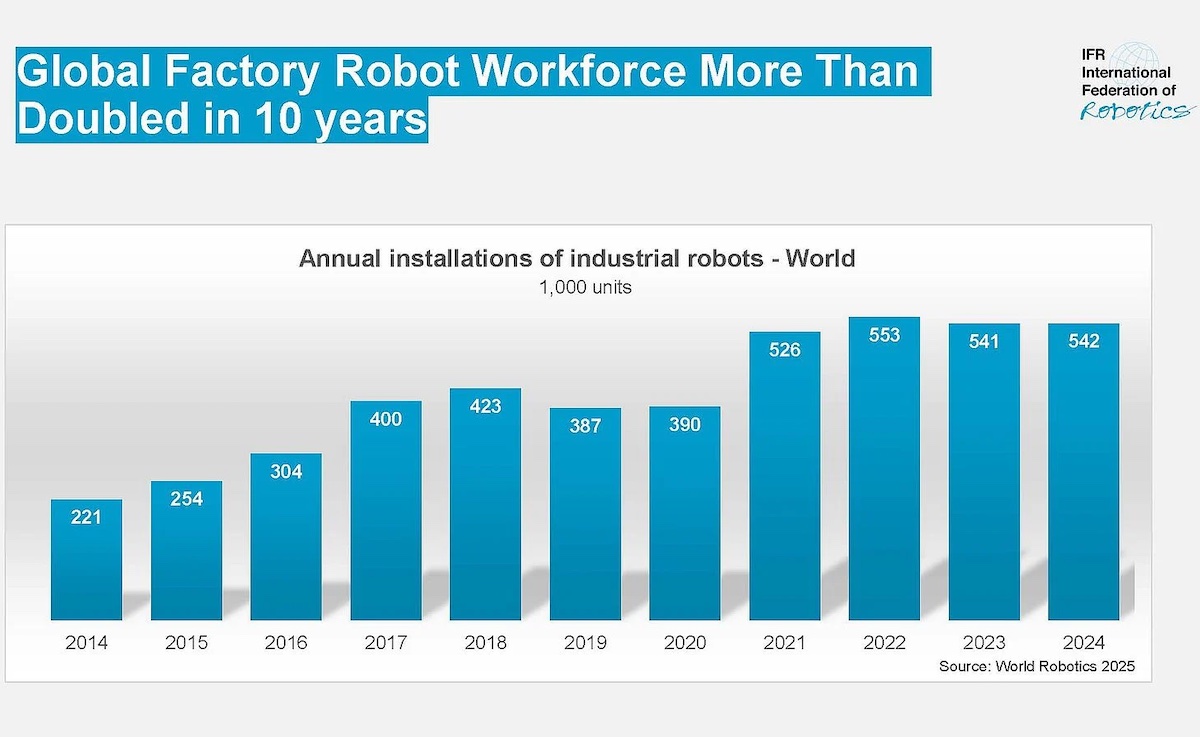

Robot adoption is rising, but the market is highly concentrated

Industrial robotics continues to expand globally, yet the latest figures in the supplied source material show a market that is far from evenly distributed. According to data cited from the International Federation of Robotics, 229,000 industrial robotic systems were sold in 2024, and 70% of those sales came from just five countries: Japan, China, the United States, Germany, and South Korea.

That concentration is one of the most important facts in the piece because it reveals how closely robotics leadership is tied to industrial policy, manufacturing capacity, and capital access. Robot adoption is clearly growing, but the benefits are accruing most heavily to countries that already have strong industrial bases and established programs to support automation ecosystems.

Industrial and service robots are diverging markets

The source text divides the wider robotics industry into industrial, professional service, and personal service segments. Each is growing, but at different scales and for different reasons. Industrial robots remain tightly linked to manufacturing productivity and modernization, while service robots increasingly reflect application-specific demand in logistics, consumer products, healthcare, and defense.

More than 343 companies worldwide manufacture industrial robots, according to the source, while more than 347 companies integrate those systems into production environments. In the service segment, more than 860 companies produce professional-use service robots and 204 make personal-use service robots. That suggests a large and still-fragmented field, especially outside the traditional industrial core.

The numbers also point to a robotics landscape where hardware alone is not the whole story. Integration, software, interfaces, autonomy, and sector-specific tailoring matter just as much as the robot arm or mobile platform itself. That helps explain why leadership in robotics can be difficult to scale quickly: success depends on a dense network of suppliers, integrators, customers, and specialized expertise.

Military and consumer uses are helping drive service growth

In the service robotics segment, the supplied text says professional-use service robot sales reached 24,207 units last year, accounting for 11.5% of the total, with military and special-purpose robots representing 45% of that volume. Personal-use service robots sold 4.7 million units, with revenue increasing 28% to $2.2 billion.

Those figures highlight a split in the sector’s momentum. Consumer-facing products can move at very large unit volumes, while professional platforms may expand through higher-value deployments in narrower applications. Defense remains an especially significant buyer in the professional segment, which can accelerate development and deployment but may also skew the direction of innovation toward specialized rather than broadly commercial use cases.

The wide variation in use cases explains why robotics is often discussed as a single market even though it behaves more like several overlapping industries. Warehouse automation, surgical systems, factory manipulators, domestic devices, and military robots share enabling technologies, but their economics and regulatory environments differ sharply.

Forecasts show large upside, but not inevitability

The source material presents ambitious outlooks for the decade ahead. The IFR expects industrial robot sales to reach 400,000 units, professional service robots to hit 152,375 units and $19.6 billion, and personal service robots to reach 35 million units and $12.2 billion. A separate projection cited from Myria Research estimates the robotics and intelligent operating systems market could exceed $380 billion by 2030.

Those forecasts underline why governments and corporations increasingly view robotics as strategic infrastructure rather than a niche automation topic. Robots touch productivity, labor availability, defense readiness, logistics resilience, and advanced manufacturing competitiveness. The countries that lead in robotics are likely to shape adjacent markets in software, sensors, power systems, and industrial AI.

Still, the source headline’s caution is justified: modernization through robotics may be needed, but it is not inevitable. High upfront costs, long integration cycles, fragmented standards, workforce adaptation, and uneven access to capital can all slow deployment. This is particularly true in sectors where processes are harder to automate or where smaller firms lack the resources to redesign operations around machines.

Why the next phase is about systems, not just machines

The most useful way to read the current market is to see robots less as standalone devices and more as nodes in a broader intelligent operating system for physical work. The source text gestures toward this with its mention of executive-level roles focused on robotics and intelligent operating systems, as well as research areas such as multimodal interfaces, self-repairing robots, energy harvesting, gesture analysis, and swarm intelligence.

That direction matters because the competitive frontier is moving beyond simple deployment counts. Future advantage will likely come from how well machines are orchestrated, updated, trained, and integrated into human workflows. A factory with a few robots is not the same as a factory built around adaptive, connected automation.

The current numbers show that robotics is no longer speculative. It is already a meaningful industrial force. But they also show that scale, concentration, and implementation barriers still define the field. The next decade will test whether robotics can spread from leading hubs into a more broadly distributed foundation for economic modernization.

This article is based on reporting by The Robot Report. Read the original article.

Originally published on therobotreport.com